Readers & Thinkers: The 2022 Nobel Prize in Economics: You’re thinking of this place all wrong – the money’s not here – [its] in Joe’s house…

Posted by ludw1086 on Oct 10, 2022 in Readers & Thinkers | Comments Off on Readers & Thinkers: The 2022 Nobel Prize in Economics: You’re thinking of this place all wrong – the money’s not here – [its] in Joe’s house…Dear All:

Well, who won?

The Nobel Prize for Economic Sciences for 2022 was announced today, October 10, 2022. It went to Ben Bernanke (former Federal Reserve chairman), Douglas Diamond, and Philip Dybvig.

Bernanke is 68 years old and was born in Augusta, Georgia. He obtained his B.A. from Harvard University and his Ph.D. from the Massachusetts Institute of Technology. His Nobel-winning work was done while an Associate Professor at Stanford University. He is currently a Distinguished Fellow in Residence at the Brookings Institution.

Diamond is 68/69 years old (his birthday is this month). He obtained his B.A. in economics from Brown University and his Ph.D. in economics from Yale University. His Nobel-winning work was done while a professor at the University of Chicago. He is currently the Merton H. Miller Distinguished Service Professor of Finance at the University of Chicago.

Dybvig is 67 years old. He obtained his undergraduate degree from Indiana University and his Ph.D. from Yale University. His Nobel-winning work was done while a professor at Yale University He is currently the Boatmen’s Bancshares Professor of Banking and Finance at Washington University in St. Louis.

The prize was given “for research on banks and financial crises”.

So what did these guys do to make them so Noble?

I often tell my students that the easiest job in the world is to run a bank. On one side, you have people giving you their money for basically free (for example, even with our high inflation, Chase offers about 0.01% interest on deposits) and you invest in all kinds of projects that pay a much higher return and you keep the difference. Some of these “projects” are really low risk, like investing in 2-year Treasury bonds that pay about 4% today. And after you make all that money, if things go wrong, the government bails you out.

For example, let’s say a typical bank takes $100 in deposits, keeps $10 in cash, and invests $90 in long-term projects (like mortgage loans, business loans, etc). Typically, the $10 is enough to give people money when they want to grab cash from their ATM card or pay bills online. The first question you might ask is whether banks are needed, why can’t the depositors just lend to the home borrowers?

Well, although probably obvious, Diamond and Dybvig showed in a simple model that banks perform a very valuable function by matching different types of investors and allowing for maturity transformation. That is, they showed that banks can match people who have low liquidity needs with those that have high liquidity needs more efficiently than other structures (primarily, because ex-ante, you don’t know which type you are). The banks allow consumers to make deposits that can be lent out for investment projects so that the economy can grow and function.

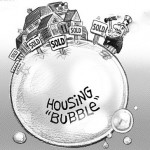

You might also wonder what happens if everyone decides to get their money from the bank on the same day. Well, clearly, there is a problem, since the bank only has a fraction of the deposits on hand ($100>$10). Thus, if everyone or even a large percentage of people withdraw from the bank on the same day, the bank will be unable to fulfill their requests. The bank could sell some of their loans, but many of the loans are illiquid in nature and it would take time to sell them and most likely they would sell them at very low prices, thus the bank would still not be able to return money to investors and would go bankrupt. What is important is that this could happen to a perfectly well managed bank with very sound assets. Diamond and Dybvig noted that in their simple model that bank runs were very possible. At the time of their writing, these ideas were known, in fact the Federal Deposit Insurance Corporation (FDIC), was created in 1933 after the bank runs of the 1930s. In that period, almost 10,000 banks failed. FDIC insurance “guarantees” that every person with a bank account will get their money back and does not have to worry about rushing to the bank to get their money before the bank runs out of money. Their model formalized what was already known by practitioners – that is, banks can fail if everyone believes that they will fail and that deposit insurance can stop bank runs. In addition to deposit insurance, Diamond and Dybvig showed that if the government acted as a lender of last resort, bank runs would also be halted. For example, the Federal Reserve could buy bank assets preventing their mark-to-market prices from being too low and this would also stabilize the financial system.

Bernanke, building on the work of Friedman and Schwartz, with verbal arguments and econometrics wrote an economic history paper about the great depression of 1929 to 1933 and argued that the financial sector played a large role in the prolongated recession. Presumably, this research, as well as lessons from the failure of Long-Term Capital Management in 1998, helped shape Bernanke’s strong response to back-up the financial system during the 2008-2009 financial crisis.

In the financial crisis of 2008-2009, a new type of bank had emerged called a Shadow Bank. These were companies like Bear Stearns, Lehman Brothers, Goldman Sachs, and so on. Although they didn’t take customer deposits like a traditional bank, they performed services that were very similar. However, these new banks did not have deposit insurance and they were not members of the Federal Reserve like major banks were. Thus, when fragility broke out in the mortgage markets, clients and customers were unsure of what could happen, and they made a run on these shadow banks. This run on shadow banks caused a self-fulfilling failure of even financially sound institutions. Because also mainstream banks did lots of mortgage lending, the bank run also occurred on commercial banks (remember Washington Mutual bank?). Eventually, the Federal Reserve did take action and acted as a lender of last resort, but before the government figured it out, many large institutions failed.

So what about the Nobel choice?

First, I didn’t expect Bernanke to win the Nobel Prize in Economics. Having said that, it is a reassuring sign for researchers. That is, even if you are not a pure theorist, but you use written arguments with some data, this can be influential. In addition to this, Bernanke put some of his research to practice as Federal Reserve Chairman, which is reassuring that applying one’s work is valued, which is often not the case in academia. I spoke to Olivier Blanchard today and he said “I was very happy about Ben’s nomination. Not only was his academic work important, but, of all economists alive, he is surely the one who has made the world a better place (or more specifically, avoided a major economic catastrophe).”

Second, Diamond and Dybvig’s model is very simple and elegant but illustrates the importance of economists in providing a framework for understanding current practice and understanding how changes to such a system might affect the economy.

Third, understanding the financial system and the economic system is incredibly important for helping human beings. At the moment, the US and other parts of the world are experiencing strong inflation that might have been ironically self-induced or maybe not. Most economists did not foresee this high inflation period in advance or at least its timing. More clarity on these issues and influencing government officials might benefit all of mankind.

So is that it?

For those who don’t know, the late Stephen Ross was the Ph.D. advisor of both Diamond and Dybvig. Although Ross never spoke about the Nobel Prize, which he should have been given, he once told me while we were having coffee in San Francisco, that he believed Diamond and Dybvig truly deserved it for their banking work. I spoke to Phil Dybvig today and he said that “…it is a real shame that Steve couldn’t be here today to see this…he would be very proud.” Unfortunately, Steve Ross died a few years ago, in which both Phil and I contributed to a special issue of the Journal of Portfolio Management.

Avinash Dixit (the Dixit of the Dixit-Stiglitz model) said the award was “…was richly deserved. Bernanke was a wonderful colleague and Chair at Princeton University.”

Implementing academic findings isn’t as easy as one would like and some questions still remain about the financial crisis of 2008. For example, while Bernanke was Fed Chairman, why didn’t the lender of last resort kick-in earlier with Bear and Lehman? During my research for the Crisis of Crowding, I was told by a CEO of a major US institution that he personally told the Fed about the risks of these institutions and their need for a lender of last resort, but the Fed replied “We can’t be preemptive”. The former Head of the BIS, Andrew Crockett, believed it was politics that prevented Bernanke from saving Bear and Lehman. Nevertheless, the Fed under Bernanke did eventually make large unprecedented efforts to restore the financial system. This was a great example of research to practice.

One morning, when Ben Bernanke was on the Council of Economic Advisors for President George Bush, he and his team had a meeting in the white house with George Bush. Bernanke was the only person who had white socks with his black shoes and President Bush made a joke about his sock mismatch. A few days later, upon the next meeting with George Bush, Bernanke had asked everyone to wear white socks to the meeting as a joke for George Bush. When President Bush entered the room, all he saw was a room full of people with legs crossed showing their mismatching white socks. After a slight pause, Bush laughed. Who knows…that joke may have led to Bush selecting him for Fed Chairman. As Ben discovered in his work on the great depression…relationships matter.

It should always be remembered that even though these three people won the prize, there are many others who have contributed to the area of banking both through research and through practice. Also, in times, like the current, where the economy is difficult for many people, we must realize that economists have a duty to persuade politicians to follow the right path, even when it isn’t the popular thing to do.

I started my blog with a joke about banking. Even so-called remedies can have unintended consequences. Deposit insurance can also create distorted incentives, like the S&L crisis of the late 1980s, just as the bailouts for big banks in 2008 and 2009 can create distorted incentives for the future. I think it was important for the Fed to intervene in the crisis of 2008, but just like raising your kids, how do you teach them to behave responsibly and prudently when they know you will bail them out when a bad event happens regardless of how they behave?

For more information on the winners:

https://www.nobelprize.org/prizes/economic-sciences/2022/press-release/

From Brookings: https://www.brookings.edu/events/ben-bernanke-awarded-nobel-prize-in-economics/

From University of Chicago: https://news.uchicago.edu/story/douglas-diamond-2022-nobel-prize-economics

From Washington University: https://source.wustl.edu/2022/10/nobel-prize-awarded-to-washu-economist-philip-dybvig/

Congratulations to Diamond, Dybvig, and Bernanke for their pursuit of knowledge, and the other armies of researchers who walked with them!

Happy Columbus Day!

Ludwig

P.S. Feel free to email me your thoughts and indicate whether you wish them to remain anonymous or not.

P.P.S. Don’t forget to watch the Silk Nobel Lecture series and sign up for future notifications. Silk Lecture Videos & www.usfnobel.com

October 10, 2022